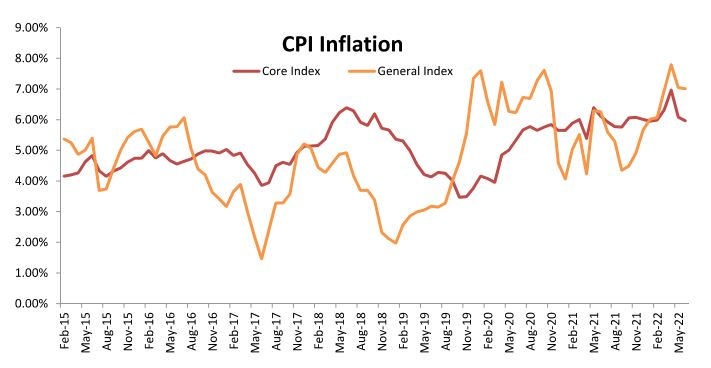

The CPI based inflation remained flattish and was reported at 7.01% for the month of Jun’22, as compared to 7.04% in the preceding month, and 6.26% during the year ago period. A favourable base effect and softness in prices of food articles led to a stable headline number. Core inflation too witnessed a move similar to the headline numbers.

The Consumer Food Price (CFP) inflation eased for the second month in a row and was reported at 7.75% for the month of Jun’22 as compared to 7.97% for the month of May’22. For the first time in months the sequential month-on-month gains in food prices lost some momentum. The components of food basket that witnessed easing of price pressures were Egg, Fruits and Pulses. The components of the food basket that reported continued inflationary pressures were Meat & Fish, Oils & Fats, Vegetables and Spices. The easing of commodity prices globally may provide a short-term relief from further gains in domestic food prices. The inflation for Clothing, Fuel & Light, Housing and Miscellaneous was reported at 9.52%, 10.39%, 3.93% and 6.28% respectively.

Fuel Price

Brent has moved down to US$ 100, and it looks set to test support levels, though the Russian invasion of Ukraine is far from over. The recent moderation has been occasioned by the fact that the US Dollar has been strengthening against all currency majors, and this should get reflected in oil prices over a period of time. It is also important to note that on the supply side it has been reported that there has been a record increase in US crude production which touched 12 million barrels per day, the highest level since 2020. The fears of an economic recession resulting from high inflation and high interest rates is also working on the mind of the markets. It may mean lower demand for oil in future. While the correction that has happened, it cannot be termed a reversal of trend, price pressures may still persist for some time. These pressures may become more severe as the Rupee continues to depreciate.

Core Inflation

Core CPI is at 5.96 % in June, as against 6.08% in the preceding month. This indicates some reduction in price pressures but not very significant. There has been easing of transport costs resulting from excise duty cuts also contributed to the lower reading. While housing prices show an uptick on a month-on-month basis, the sequential growth is lower. Healthcare, education, personal care and effects, recreation and amusement have moved up and they may have the effect of keeping the core number stickier, and therefore, inflationary trend in these components is likely to be sustained.

Outlook

Inflationary pressures may moderate but could still remain at relatively elevated levels, hovering around the ceiling of the RBI target. This would imply the need to keep the pressure on inflation through rate action by the central bank till prices fall and settle within the target ranges. The RBI has shifted the focus from growth sustaining to inflation fighting in the last three policy announcements. Since inflation control remains a priority, rate action is inevitable, but the quantum of the rate hike may depend on the macro numbers available from time to time.