The GDP growth number for Q4FY21 was reported at 1.6% as compared to 0.5% in the preceding quarter. The GDP for FY21 was reported at -7.3%, largely reflecting the pandemic driven impact to the economy. The GVA number for Q4FY21 came in at 3.7% as compared to 1% in the preceding quarter. The yearly growth estimates as per the GVA calculation were reported at -6.2%. The quarterly growth rates have shown sequential improvement and have been better than street estimates. The yearly growth rate is reflective of the hit Indian economy took in the wake of the pandemic and the resultant lockdowns. The days of the negative growth may be behind us and the quarterly growth rates have returned to positive terrain, after the sharp contraction in economic activity witnessed during the first two quarters of FY21.

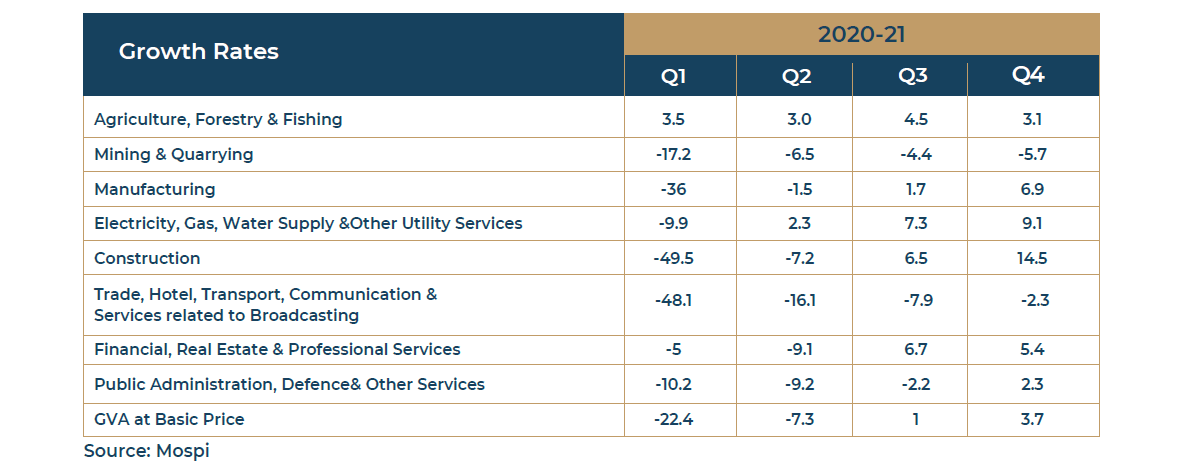

As has been the case for the last 8 quarters, agricultural activities reported robust growth and has been a key support to the headline GVA numbers. The growth for agriculture and allied activities was reported at 3.1% for Q4FY21. The industrial activity continued to improve in Q4FY21, the growth rate was reported at 7.9% in the latest quarter as compared to 2.9% in the preceding one. Within industry, the growth continued to remain in contraction zone for mining (-5.7%) as was the case even before the pandemic. The other components of industry viz, manufacturing (6.9%), electricity (9.1%) and construction (14.5%) reported healthy growth rates. The improvements in manufacturing and industry are already quite visible in the corporate performance reported in the last two sets of quarterly earnings results. On the other hand, services sector continued to witness suppressed activity levels in Q4FY21. The sub-components within the services sector reported divergent growth rates depending on the nature of services offered. While trade, hotel and transportation (-2.3%) continued to face the brunt of restricted and cautious people movement, the finance and real estate services (5.4%) did relatively better. Public administration, defence and other services, partly representative of government expenditure, reverted back to growth trajectory with growth rate reported at 2.3% as compared to -2.2% in the preceding quarter

All the sub-components on the expenditure witnessed an uptrend but the strength of the growth numbers was a mixed bag. The critical component of Private Consumption Expenditure reported a relatively weaker growth rate of 2.7%, an improvement though from the contraction seen over the last three quarters. Another crucial component, Gross Fixed Capital Formation has reported growth rate of 10.9% as compared to 2.6% in the preceding quarter. It is important to sustain this momentum in capital formation from the perspective of supporting a sustained upward trajectory of headline growth numbers. The government consumption expenditure too has picked up well and reported a growth rate of 28.3%, given the weakness in private consumption it is expected that government expenditure will continue to be supportive.

The latest growth numbers are indicative of the strength gained by the economy during the last two quarters as the country was coming out of the pandemic induced lockdowns. Even as the GDP contracted by 24.4% in the first quarter of FY21, economy recovered fairly quickly as the severity of the first wave dissipated and also as it received effective support from both monetary and fiscal policy. We believe the growth trajectory for FY22 may remain similar to the one witnessed in FY21. The growth numbers may be closely linked to the spread of the pandemic and the success of the measures to contain it.

The incidence of the second wave of the pandemic led to similar measures as were implemented during the previous fiscal to control the spread. The private consumption demand may continue to get affected by the localised lockdowns and may witness only a gradual recovery. This time around as the manufacturing activity has been permitted to continue to operate, this segment would continue to be one of the key engines of growth. The second key supportive factor would be the government expenditure, both on the revenue as well as the capital side. The third and the most important factor would be the speed of the vaccination program. Over the recent past, supply related issues had impacted the pace of the vaccine drive, if the supply is ramped-up in time it would play an important role in a swift growth revival. Given the strength of the second wave, we believe the growth concerns are not completely behind, and the economy would continue to require monetary and fiscal support, at least over the next two quarters.