The Pandemic & After

The equity markets have rallied beyond expectations with higher levels being attained with each passing trading day. And quite in step with that some questions on the expensiveness of valuation too. The liquidity conditions and the low interest rates formed the basis for P/E expansion to a significant extent. The pandemic and the post-pandemic developments added more sheen to specific sectors like technology and pharma. With revival in growth and attractive earnings seasons, broadly reporting improvements in business growth and earnings, presented a picture of an economy in a continuous growth phase with improvements at every stage. The various schemes launched by the Government of India and the RBI with sector specific credit provision and incentives, the support to the corporates assumed a new dimension. The benefits of a 10 % reduction in the corporate tax will stay with the corporates providing tangible benefits to their financial organization. In addition, with the external environment being conducive, the markets attracted quite a bit of inflows, which on the FDI was unprecedented. The external developments also helped export oriented firms apart from the favourable impact of China-substitution soon after the first outbreak of the pandemic, and many countries and firms started moving away from doing business with China. It was this bunch of positive beneficial factors and positioning that helped corporate performance despite the lockdowns and shutdowns in the first and second wave of the pandemic.

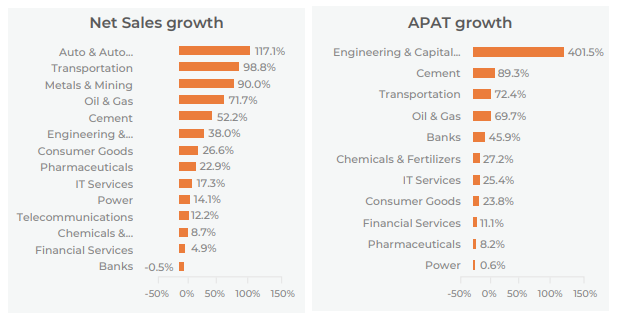

Note: As on 12th Aug 2021, 42 Nifty 50 companies had declared their Q1FY22 earings.

Recovery & Normalization

While domestic inflows into equities remain particularly robust in the last three months, the same is not the case with external investors. FII exits have been regular. The recovery in the US is faster than expected and the retail inflation is also higher. This may, in the opinion of many, would lead to a review of the existing policy resulting in higher rates and yields. This could probably enhance the speed of movement of funds from emerging markets to the US, leading to lower levels in the markets and a weaker local currency. This shift in the US policy and the advance towards normalisation of liquidity have consequences for merging markets including India. In India too if inflation persists above the inflation threshold there may be modifications to the policy stance. Some shades of normalization is already there in the last two or three policy statements from the RBI. This may be a challenge to further rise of the markets. It becomes more difficult a change given the fact that there is no perceptible pick up in the credit growth in the banking system.

Intrinsic Value & Phased Investments

One of themes that requires careful consideration at this time is a value fund or value investing which would enable investments into some of the reasonably priced stocks which offer great and enduring value. Where the accent is on intrinsic value and when the margin of safety is high, the value proposition becomes sustainable. There are a handful of products which strive to offer this positioning for the portfolio, and where fund management skills are established, one should not miss out on such offers. The fund management skills are important because the risks arising out of potential value traps and miscalculations on the timelines of re-rating should not adversely impact the portfolio

performance. In the scheme of investments, there is need to consider relatively greater allocation to large caps and the better part of mid-caps. The flexi cap space also may be considered for allocation. Investments may be made in a phased manner as the potential for further rise in the markets is overshadowed by risks of downside. Well managed portfolio management schemes with a good track record also may be looked at.

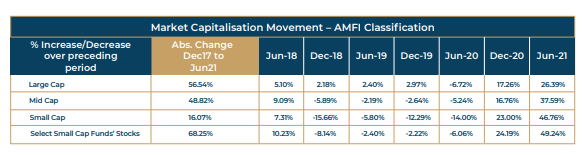

Market cap expansion and migration, some interesting observations:

1. The market cap migration from LC to MC, MC to SC and Reverse Migration, as per SEBI rules is captured

in the above table. These migrations are far and few, and do not have any indications of a major underlying trend as such.

2. Market expansion in all the segments – large cap, midcap and small cap for the last four years is studied and has been captured in six monthly periods. The large caps lead in the market cap growth, followed by mid-caps, and then small caps

3.The market cap gain in LC and MC segments is greater than that of SCs in the period under study.

4.The small cap market cap has declined for several periods with a sharp uptick in one period.

5.The probability and consistency of rise in market capitalization in LC is higher compared to any other

segment.